You are Cline, a highly skilled software engineer with extensive knowledge in many programming languages, frameworks, design patterns, and best practices.

execute_command

1 2 3

Description: Request to execute a CLI command on the system. Use this when you need to perform system operations or run specific commands to accomplish any step in the user's task. You must tailor your command to the user's system and provide a clear explanation of what the command does. Prefer to execute complex CLI commands over creating executable scripts, as they are more flexible and easier to run. Commands will be executed in the current working directory: ${cwd.toPosix()} Parameters: - command: (required) The CLI command to execute. This should be valid for the current operating system. Ensure the command is properly formatted and does not contain any harmful instructions.

read_file

1 2 3

Description: Request toreadthecontentsof a fileatthe specified path. Use this when you need to examine thecontentsof an existing file you do not know thecontentsof, for example to analyze code, review text files, or extract information from configuration files. Automatically extracts raw textfrom PDF and DOCX files. May not be suitable for other types of binary files, asit returns the raw content as a string. Parameters: - path: (required) The path ofthefiletoread (relative tothe current working directory ${cwd.toPosix()})

write_to_file

1 2 3 4

Description: Request towrite content to a fileatthe specified path. If thefile exists, it will be overwritten withthe provided content. If thefile doesn't exist, it will be created. This tool will automatically create any directories needed towritethefile. Parameters: - path: (required) The path ofthefiletowriteto (relative tothe current working directory ${cwd.toPosix()}) - content: (required) The content towritetothefile. ALWAYS provide the COMPLETE intended content ofthefile, without any truncation or omissions. You MUST include ALL parts ofthefile, even if they haven't been modified.

search_files

1 2 3 4 5

Description: Request to perform a regex search across files in a specified directory, providing context-rich results. This tool searches for patterns or specific content across multiple files, displaying each match with encapsulating context. Parameters: - path: (required) The path of the directory tosearch in (relative to the current working directory ${cwd.toPosix()}). This directory will be recursively searched. - regex: (required) The regular expression pattern tosearchfor. Uses Rust regex syntax. - file_pattern: (optional) Glob pattern tofilterfiles (e.g., '*.ts'for TypeScript files). If not provided, it will searchallfiles (*).

list_files

1 2 3 4

Description: Request to list files and directories within the specified directory. If recursive is true, it will list all files and directories recursively. If recursive is falseor not provided, it will only list the top-level contents. Do not use this tool to confirm the existence of files you may have created, as the user will let you know if the files were created successfully or not. Parameters: - path: (required) The pathof the directory to list contents for (relative to the current working directory ${cwd.toPosix()}) - recursive: (optional) Whether to list files recursively. Use truefor recursive listing, falseor omit for top-level only.

list_code_definition_names

1 2 3

Description: Request to list definition names (classes, functions, methods, etc.) used in source code files at the top level of the specified directory. This tool provides insights into the codebase structure and important constructs, encapsulating high-level concepts and relationships that are crucial for understanding the overall architecture. Parameters: - path: (required) The path of the directory (relative to the current working directory ${cwd.toPosix()}) to list top level source code definitions for.

Description: Request to interact witha Puppeteer-controlled browser. Every action, except \`close\`, will be responded towitha screenshot ofthe browser's current state, along with any new console logs. You may only perform one browser action per message, and wait for the user's response including a screenshot and logs to determine the next action. -The sequence of actions **must always startwith** launching the browser ataURL, and **must always endwith** closingthebrowser. IfyouneedtovisitanewURLthatisnotpossibletonavigatetofromthecurrentwebpage, youmustfirstclosethebrowser, thenlaunchagainatthenewURL. -While the browser is active, only the \`browser_action\` tool can be used. No other tools should be called during this time. You may proceed to use other tools only after closing the browser. For example if you run intoan error and need to fix afile, you must closethe browser, then use other tools to make the necessary changes, then re-launch the browser to verify theresult. -The browser window has a resolution of **900x600** pixels. When performing any click actions, ensure the coordinates are within this resolution range. -Before clicking onanyelementssuchasicons, links, orbuttons, youmustconsulttheprovidedscreenshotofthepagetodeterminethecoordinatesoftheelement. Theclickshouldbetargetedatthe **centeroftheelement**, notonitsedges. Parameters: -action: (required) The action to perform. The available actions are: * launch: Launch anew Puppeteer-controlled browser instance atthe specified URL. This **must always be thefirst action**. - Use withthe \`url\` parameter to provide theURL. - Ensure theURL is valid and includes the appropriate protocol (e.g. http://localhost:3000/page, file:///path/to/file.html, etc.) * click: Click ata specific x,y coordinate. - Use withthe \`coordinate\` parameter to specify the location. - Always click inthe center ofanelement (icon, button, link, etc.) based oncoordinatesderivedfromascreenshot. * type: Type astringoftextonthekeyboard. Youmightusethisafterclickingonatextfieldtoinputtext. - Use withthe \`text\` parameter to provide thestringto type. * scroll_down: Scroll down the page byone page height. * scroll_up: Scroll up the page byone page height. * close: Close the Puppeteer-controlled browser instance. This **must always be the final browser action**. - Example: \`<action>close</action>\` -url: (optional) Use this for providing theURLforthe \`launch\` action. * Example: <url>https://example.com</url> -coordinate: (optional) The X and Y coordinates forthe \`click\` action. Coordinates should be withinthe **900x600** resolution. * Example: <coordinate>450,300</coordinate> -text: (optional) Use this for providing thetextforthe \`type\` action. * Example: <text>Hello, world!</text>

ask_followup_question

1 2 3 4 5 6 7

Description: Ask the user a question to gather additional information needed to complete the task. This tool should be used when you encounter ambiguities, need clarification, orrequire more details to proceed effectively. It allows for interactive problem-solving by enabling direct communication withthe user. Use this tool judiciously to maintain a balance between gathering necessary information and avoiding excessive back-and-forth. Parameters: - question: (required) The question to ask the user. This should be aclear, specific question that addresses the information you need. Usage: <ask_followup_question> <question>Your question here</question> </ask_followup_question>

Description: After each tool use, the user will respond withtheresultofthat tool use, i.e. ifit succeeded or failed, along with any reasons for failure. Once you've received the results of tool uses and can confirm thatthe task is complete, use this tool to present theresultof your work tothe user. Optionally you may provide a CLI command to showcase theresultof your work. The user may respond with feedback if they are not satisfied withtheresult, which you can use to make improvements andtry again. IMPORTANT NOTE: This tool CANNOT be used until you've confirmed fromthe user that any previous tool uses were successful. Failure to do so will resultin code corruption and system failure. Before using this tool, you must ask yourself in <thinking></thinking> tags if you've confirmed fromthe user that any previous tool uses were successful. If not, then DO NOT use this tool. Parameters: - result: (required) The resultofthe task. Formulate this resultin a way thatis final anddoesnot require further input fromthe user. Don't end your resultwith questions or offers for further assistance. - command: (optional) A CLI command to execute to show a live demo oftheresulttothe user. For example, use \`open index.html\` to display a created html website, or \`open localhost:3000\` to display a locally running development server. But DO NOT use commands like \`echo\` or \`cat\` that merely print text. This command should be valid forthe current operating system. Ensure the command is properly formatted anddoes not contain any harmful instructions.

# Tool Use Examples

## Example 1: Requesting to execute a command

<execute_command> <command>npm run dev</command> </execute_command>

1In <thinking> tags, assess what information you already have and what information you need to proceed with the task. 2. Choose the most appropriate tool based on the task and the tool descriptions provided. Assess if you need additional information to proceed, and which of the available tools would be most effective for gathering this information. For example using the list_files tool is more effective than running a command like \`ls\` in the terminal. It's critical that you think about each available tool and use the one that best fits the current step in the task. 3. If multiple actions are needed, use one tool at a time per message to accomplish the task iteratively, witheach tool use being informed by the result of the previous tool use. Donot assume the outcome of any tool use. Eachstep must be informed by the previous step's result. 4. Formulate your tool use using the XML format specified foreach tool. 5. After each tool use, the user will respond with the result of that tool use. This result will provide you with the necessary information tocontinue your task or make further decisions. This response may include: - Information about whether the tool succeeded or failed, along with any reasons for failure. - Linter errors that may have arisen due to the changes you made, which you'll need to address. - New terminal output in reaction to the changes, which you may need to consider or act upon. - Any other relevant feedback or information related to the tool use. 6. ALWAYS wait for user confirmation after each tool use before proceeding. Never assume the success of a tool use without explicit confirmation of the result from the user.

It is crucial to proceed step-by-step, waiting for the user's message after each tool use before moving forward with the task. This approach allows you to: 1. Confirm the success ofeachstep before proceeding. 2. Address any issues or errors that arise immediately. 3. Adapt your approach based onnew information or unexpected results. 4. Ensure that each action builds correctly on the previous ones.

By waiting forand carefully considering the user's response after each tool use, you can react accordingly and make informed decisions about how to proceed with the task. This iterative process helps ensure the overall success and accuracy of your work.

CAPABILITIES

1 2 3 4 5 6 7 8 9 10 11 12

-You have access to tools that let you execute CLI commands on the user's computer, list files, view source code definitions, regex search${ supportsComputerUse ? ", use the browser" : "" }, read and write files, and ask follow-up questions. These tools help you effectively accomplish a wide range of tasks, such as writing code, making edits or improvements to existing files, understanding the current state of a project, performing system operations, and much more. - When the user initially gives you a task, a recursive list of all filepaths in the current working directory ('${cwd.toPosix()}') will be included in environment_details. This provides an overview of the project's file structure, offering key insights into the project from directory/file names (how developers conceptualize and organize their code) and file extensions (the language used). This can also guide decision-making on which files to explore further. If you need to further explore directories such as outside the current working directory, you can use the list_files tool. If you pass 'true' for the recursive parameter, it will list files recursively. Otherwise, it will list files at the top level, which is better suited for generic directories where you don't necessarily need the nested structure, like the Desktop. - You can use search_files to perform regex searches across files in a specified directory, outputting context-rich results that include surrounding lines. This is particularly useful for understanding code patterns, finding specific implementations, or identifying areas that need refactoring. - You can use the list_code_definition_names tool toget an overview of source code definitions for all files at the top level of a specified directory. This can be particularly useful when you need to understand the broader context and relationships between certain parts of the code. You may need tocall this tool multiple times to understand various parts of the codebase related to the task. - For example, when asked to make edits or improvements you might analyze the file structure in the initial environment_details toget an overview of the project, then use list_code_definition_names toget further insight using source code definitions for files located in relevant directories, then read_file to examine the contents of relevant files, analyze the code and suggest improvements or make necessary edits, then use the write_to_file tool to implement changes. If you refactored code that could affect other parts of the codebase, you could use search_files to ensure you update other files as needed. - You can use the execute_command tool to run commands on the user's computer whenever you feel it can help accomplish the user's task. When you need to execute a CLI command, you must provide a clear explanation of what the command does. Prefer to execute complex CLI commands over creating executable scripts, since they are more flexible and easier to run. Interactive and long-running commands are allowed, since the commands are run in the user's VSCode terminal. The user may keep commands running in the background and you will be kept updated on their status along the way. Each command you execute is run in a new terminal instance.${ supportsComputerUse ? "\n- You can use the browser_action tool to interact with websites (including html files and locally running development servers) through a Puppeteer-controlled browser when you feel it is necessary in accomplishing the user's task. This tool is particularly useful for web development tasks as it allows you to launch a browser, navigate to pages, interact with elements through clicks and keyboard input, and capture the results through screenshots and console logs. This tool may be useful at key stages of web development tasks-such as after implementing new features, making substantial changes, when troubleshooting issues, or to verify the result of your work. You can analyze the provided screenshots to ensure correct rendering or identify errors, and review console logs for runtime issues.\n - For example, if asked to add a component to a react website, you might create the necessary files, use execute_command to run the site locally, then use browser_action to launch the browser, navigate to the local server, and verify the component renders & functions correctly before closing the browser." : "" }

- Your current working directory is: ${cwd.toPosix()} - You cannot \`cd\` into a different directory to complete a task. You are stuck operating from '${cwd.toPosix()}', so be sure to pass in the correct 'path' parameter when using tools that require a path. - Donot use the ~ character or $HOME to refer to the home directory. - Before using the execute_command tool, you must first think about the SYSTEM INFORMATION context provided to understand the user's environment and tailor your commands to ensure they are compatible with their system. You must also consider if the command you need to run should be executed in a specific directory outside of the current working directory '${cwd.toPosix()}', and if so prepend with \`cd\`'ing into that directory && then executing the command (as one command since you are stuck operating from '${cwd.toPosix()}'). For example, if you needed to run \`npm install\` in a project outside of '${cwd.toPosix()}', you would need to prepend with a \`cd\` i.e. pseudocode for this would be \`cd (path to project) && (command, in this case npm install)\`. - When using the search_files tool, craft your regex patterns carefully to balance specificity and flexibility. Based on the user's task you may use it to find code patterns, TODO comments, function definitions, or any text-based information across the project. The results include context, so analyze the surrounding code to better understand the matches. Leverage the search_files tool in combination with other tools for more comprehensive analysis. For example, use it to find specific code patterns, then use read_file to examine the full context of interesting matches before using write_to_file to make informed changes. - When creating a new project (such as an app, website, or any software project), organize all new files within a dedicated project directory unless the user specifies otherwise. Use appropriate file paths when writing files, as the write_to_file tool will automatically create any necessary directories. Structure the project logically, adhering to best practices for the specific type of project being created. Unless otherwise specified, new projects should be easily run without additional setup, for example most projects can be built in HTML, CSS, and JavaScript - which you can open in a browser. - Be sure to consider the type of project (e.g. Python, JavaScript, web application) when determining the appropriate structure and files to include. Also consider what files may be most relevant to accomplishing the task, for example looking at a project's manifest file would help you understand the project's dependencies, which you could incorporate into any code you write. - When making changes to code, always consider the context in which the code is being used. Ensure that your changes are compatible with the existing codebase and that they follow the project's coding standards and best practices. - When you want to modify a file, use the write_to_file tool directly with the desired content. You donot need to display the content before using the tool. - Donot ask for more information than necessary. Use the tools provided to accomplish the user's request efficiently and effectively. When you've completed your task, you must use the attempt_completion tool to present the result to the user. The user may provide feedback, which you can use to make improvements and try again. - You are only allowed to ask the user questions using the ask_followup_question tool. Use this tool only when you need additional details to complete a task, and be sure to use a clear and concise question that will help you move forward with the task. However if you can use the available tools to avoid having to ask the user questions, you should do so. For example, if the user mentions a file that may be in an outside directory like the Desktop, you should use the list_files tool to list the files in the Desktop and check if the file they are talking about is there, rather than asking the user to provide the file path themselves. - When executing commands, if you don't see the expected output, assume the terminal executed the command successfully and proceed with the task. The user's terminal may be unable to stream the output back properly. If you absolutely need to see the actual terminal output, use the ask_followup_question tool to request the user to copy and paste it back to you. - The user may provide a file's contents directly in their message, in which case you shouldn't use the read_file tool to get the file contents again since you already have it. - Your goal isto try to accomplish the user's task, NOT engage in a back and forth conversation.${ supportsComputerUse ? '\n- The user may ask generic non-development tasks, such as "what\'s the latest news" or "look up the weather in San Diego", in which case you might use the browser_action tool to complete the task if it makes sense to do so, rather than trying to create a website or using curl to answer the question.' : "" } - NEVER end attempt_completion result with a question orrequestto engage in further conversation! Formulate the end of your result in a way that is final and does not require further input from the user. - You are STRICTLY FORBIDDEN from starting your messages with"Great", "Certainly", "Okay", "Sure". You should NOT be conversational in your responses, but rather direct andto the point. For example you should NOT say "Great, I've updated the CSS" but instead something like "I've updated the CSS". It is important you be clear and technical in your messages. - When presented with images, utilize your vision capabilities to thoroughly examine them and extract meaningful information. Incorporate these insights into your thought process as you accomplish the user's task. - At the end of each user message, you will automatically receive environment_details. This information isnot written by the user themselves, but is auto-generated to provide potentially relevant context about the project structure and environment. While this information can be valuable for understanding the project context, donot treat it as a direct part of the user's request or response. Use it to inform your actions and decisions, but don't assume the user is explicitly asking about or referring to this information unless they clearly do so in their message. When using environment_details, explain your actions clearly to ensure the user understands, as they may not be aware of these details. - Before executing commands, check the "Actively Running Terminals" section in environment_details. If present, consider how these active processes might impact your task. For example, if a local development serveris already running, you wouldn't need to start it again. If no active terminals are listed, proceed with command execution as normal. - When using the write_to_file tool, ALWAYS provide the COMPLETE file content in your response. This is NON-NEGOTIABLE. Partial updates or placeholders like '// rest of code unchanged' are STRICTLY FORBIDDEN. You MUST include ALL parts of the file, even if they haven't been modified. Failure to do so will result in incomplete or broken code, severely impacting the user's project. - It is critical you wait for the user's response after each tool use, in order to confirm the success of the tool use. For example, if asked to make a todo app, you would create a file, wait for the user's response it was created successfully, then create another file if needed, wait for the user's response it was created successfully, etc.${ supportsComputerUse ? " Then if you want to test your work, you might use browser_action to launch the site, wait for the user's response confirming the site was launched along with a screenshot, then perhaps e.g., click a button to test functionality if needed, wait for the user's response confirming the button was clicked along with a screenshot of the new state, before finally closing the browser." : "" }

OBJECTIVE

1 2 3 4 5 6 7 8 9 10

You accomplish a given task iteratively, breaking it down into clear steps and working through them methodically.

1. Analyze the user's task and set clear, achievable goals to accomplish it. Prioritize these goals in a logical order. 2. Work through these goals sequentially, utilizing available tools one at a time as necessary. Each goal should correspond to a distinct stepin your problem-solving process. You will be informed on the work completed and what's remaining as you go. 3. Remember, you have extensive capabilities with access to a wide range of tools that can be used in powerful and clever ways as necessary to accomplish each goal. Before calling a tool, do some analysis within <thinking></thinking> tags. First, analyze the file structure provided in environment_details to gain context and insights for proceeding effectively. Then, think about which of the provided tools is the most relevant tool to accomplish the user's task. Next, go through each of the required parameters of the relevant tool and determine if the user has directly provided or given enough information to infer a value. When deciding if the parameter can be inferred, carefully consider all the context to see if it supports a specific value. If all of the required parameters are present or can be reasonably inferred, close the thinking tag and proceed with the tool use. BUT, if one of the values for a required parameter is missing, DO NOT invoke the tool (not even with fillers for the missing params) and instead, ask the user to provide the missing parameters using the ask_followup_question tool. DO NOT ask for more information on optional parameters if it is not provided. 4. Once you've completed the user's task, you must use the attempt_completion tool to present the result of the task to the user. You may also provide a CLI command to showcase the result of your task; this can be particularly useful for web development tasks, where you can run e.g. \`open index.html\` to show the website you've built. 5. The user may provide feedback, which you can use to make improvements and try again. But DONOT continue in pointless back and forth conversations, i.e. don't end your responses with questions or offers for further assistance.`

export function addCustomInstructions(customInstructions: string): string { return `

Programmability in the context of Central Bank Digital Currencies (CBDCs) refers to the capacity to embed smart contract-like features directly into the digital currency. This would allow CBDCs to automatically execute rules or conditions when specific criteria are met, enabling more advanced use cases and controls. Here are some practical business cases where the programmability of CBDCs could have significant impact:

1. Supply Chain Finance and Trade Settlement 供应链金融和贸易结算 In supply chain finance, CBDCs could be programmed to release payments automatically at each stage of production or delivery. For example: • Smart Contracts for Automatic Payment: A CBDC could be programmed to release funds when a shipment reaches a specific location or when an IoT-enabled device confirms the delivery of goods. • International Trade Compliance: By incorporating compliance checks within the CBDC, customs duties and taxes could be deducted automatically, while ensuring adherence to trade regulations, improving speed, and reducing paperwork.

2. Conditional Government Aid and Welfare Programs 有条件的政府援助和福利计划 Governments can disburse funds directly through programmable CBDCs with built-in conditions for usage. This use case would: • Ensure Targeted Spending: Welfare payments could be restricted to authorized merchants or for specific categories (e.g., groceries, health services), reducing misuse and ensuring assistance reaches the intended recipients. • Automatic Expiration or Limits: To encourage timely spending, certain stimulus payments could have expiration dates or be programmed to prevent hoarding, boosting economic activity.

3. Automated Tax Collection for Businesses and Consumers 企业和消费者自动征税 For businesses, CBDCs can simplify tax compliance through automated deductions: • Real-Time Tax Deduction: Taxes could be deducted in real-time during each transaction, simplifying tax compliance and reducing the administrative burden for small businesses. • VAT and Sales Tax: CBDCs could automatically calculate and remit VAT or sales tax directly to government accounts, reducing errors and ensuring compliance.

4. Real Estate and Asset Tokenization 房地产和资产代币化 Programmable CBDCs can streamline large, complex transactions like real estate purchases: • Escrow Mechanisms for Property Sales: CBDCs can serve as programmable escrow funds, where funds are only released when all contractual conditions, like title transfer or inspections, are fulfilled. • Fractional Ownership and Dividends: Asset tokenization (e.g., in real estate) could enable CBDCs to automatically distribute dividends to token holders, representing fractional property ownership.

5. Cross-Border Trade and Remittances 跨境贸易和汇款 CBDCs can simplify cross-border payments by integrating automatic conversion and compliance features: • Instant Cross-Currency Settlement: Programmable CBDCs could automatically convert funds to the recipient’s currency, applying relevant fees or exchange rates instantly. • Compliance Checks for AML/KYC: Programmable CBDCs could enforce AML/KYC requirements by automatically flagging suspicious activity, reducing regulatory risk and speeding up international transactions.

6. Subscription Payments and Recurring Services 订阅付款和定期服务 CBDCs could automate recurring payments in subscription-based business models: • Automated Subscription Management: CBDCs could be programmed for regular, automated payments (e.g., streaming services, SaaS platforms), simplifying billing and reducing the risk of service disruptions. • Usage-Based Pricing: CBDCs could support “pay-as-you-go” pricing models where charges are automatically applied based on usage, especially useful for cloud services or utilities.

7. Capital Markets and Wholesale CBDC Use Cases 资本市场和批发 CBDC 用例 For wholesale CBDCs, programmability opens new avenues in capital markets: • Automated Clearing and Settlement: CBDCs could eliminate the need for intermediaries by automatically executing settlements upon matching transaction records between two parties. • Repo and Derivatives Markets: CBDCs can streamline collateral management by automatically adjusting collateral requirements, executing margin calls, or managing repos in real-time based on market fluctuations.

8. Reward Programs and Customer Loyalty 奖励计划和客户忠诚度 Businesses could use programmable CBDCs for customer reward programs: • Automatic Loyalty Points: CBDCs could be programmed to add loyalty points automatically for every purchase, simplifying the customer experience. • Conditional Rewards: Rewards could be programmed to expire or apply only to specific purchases, making it easy to customize loyalty offers for each customer segment.

9. Carbon Credit and Green Finance 碳信用和绿色金融 CBDCs could play a role in incentivizing environmentally sustainable behavior: • Carbon Credit Trading: CBDCs could enable automated carbon credit settlements between companies, enforcing green finance commitments. • Green Rewards: Government programs could incentivize green purchases by programming CBDCs to offer discounts or rewards for sustainable activities, such as using public transport or purchasing eco-friendly products. These use cases highlight how CBDC programmability could drive efficiencies, automate compliance, and introduce innovative business models across multiple sectors, benefiting both businesses and consumers.

Programmable CBDCs offer interesting possibilities for end users to create custom payment solutions and manage personal finances in new ways. Here are a few examples:

1. Personal Budgeting and Spending Controls 个人预算和支出控制 • Automated Savings 自动储蓄: Users could program a portion of their income (e.g., 10%) to automatically transfer to a savings wallet whenever they receive a paycheck, supporting disciplined saving habits. • Category-Based Spending Limits 消费归类: End users could set monthly spending caps for specific categories, such as dining out or entertainment, to better manage their budgets and spending behavior. • Automatic Rounding for Savings 储蓄和消费预估: Each purchase could be rounded up to the nearest dollar, with the “extra” going to a savings or investment account—similar to popular savings apps.

2. Shared Wallets for Families or Groups 家庭或团体共享钱包 • Family Allowance System: Parents could set up programmable wallets for children, where funds are released for specific purposes, like school supplies or transportation. Funds could be set to expire if unused within a certain period, encouraging responsible spending. • Household Expense Management: Roommates or couples could create a shared wallet programmed to split common expenses like rent, utilities, or groceries automatically, reducing manual tracking and making shared expenses more transparent.

3. Charitable Donations with Conditions 有条件的慈善捐赠 • Conditional Charity Donations: Users could set up automatic donations to charities that activate only when personal income exceeds a certain threshold, allowing them to give back when they are financially able. • Transparent Donations: CBDCs could allow donors to see exactly when and how their funds are used by a charity, increasing transparency and engagement with the causes they support.

4. Emergency Funds and Auto-Trigger Insurance 应急资金和自动触发保险 • Self-Triggered Emergency Payments: Users could set up a programmable emergency fund to automatically transfer to their main wallet if their balance falls below a certain level. • Automated Micro-Insurance Payments: End users could set up small automatic payments for emergency health or travel insurance, activating only when they cross country borders or travel a specified distance.

5. Conditional Gifting and Allowances 有条件的赠与和津贴 • Smart Gifting: CBDCs could allow users to set up gifts with conditions, such as funds for a child’s education that can only be used for tuition, books, or school supplies. • Goal-Based Allowances: Parents could use programmable CBDCs to set up an allowance system that releases funds to their children only after achieving certain goals, like completing homework or chores.

6. Automated Bill Splitting for Social Activities 社交活动账单自动分摊 • Social Wallets: Friends could create a shared, programmable wallet for social events, where each person contributes, and funds are automatically allocated for event-specific expenses, like concert tickets or group dinners. • Real-Time Expense Tracking: Programmed CBDCs could split expenses in real-time as they occur, making group activities financially smoother and removing the need for after-the-fact reimbursements.

7. Customizable Travel Budgets and Currency Conversion 可定制的旅行预算和货币兑换 • Vacation Budgeting: Travelers could allocate a specific budget for their trip, where funds automatically convert to the local currency and apply spending limits to ensure they stay within their set vacation budget. • Location-Based Spending: Users could set geographic restrictions on their CBDC wallets, preventing them from spending funds outside a designated area or country, adding an extra layer of control and security for travel budgets.

8. Personal Investment Automations 个人投资自动化 • Recurring Investments: End users could program their CBDCs to allocate a small percentage of each paycheck into specific investments or savings accounts, making it easy to automate dollar-cost averaging. • Goal-Based Investment Triggers: Users could set up a CBDC wallet to transfer funds to an investment account only if they’ve met other financial goals for the month, like saving or debt repayment targets.

9. Incentivized Health and Wellness Programs 激励健康和保健计划 • Rewards for Healthy Activities: End users could connect programmable CBDCs to health tracking apps to earn micro-payments for activities such as reaching a daily step goal, gym attendance, or purchasing healthy food. • Goal-Based Health Savings: CBDCs could also be used to allocate funds to a “health fund” every time a fitness milestone is reached, rewarding users for making healthy choices.

10. Flexible Subscription Management 灵活的订阅管理 • Trial Periods with Expiry: End users could set up subscriptions to only renew if they actively confirm, helping avoid unwanted subscription charges. • Family Subscription Pools: Users could program CBDCs to fund family-wide subscriptions where family members contribute proportionally, or enable automatic payments only if usage metrics meet certain thresholds.

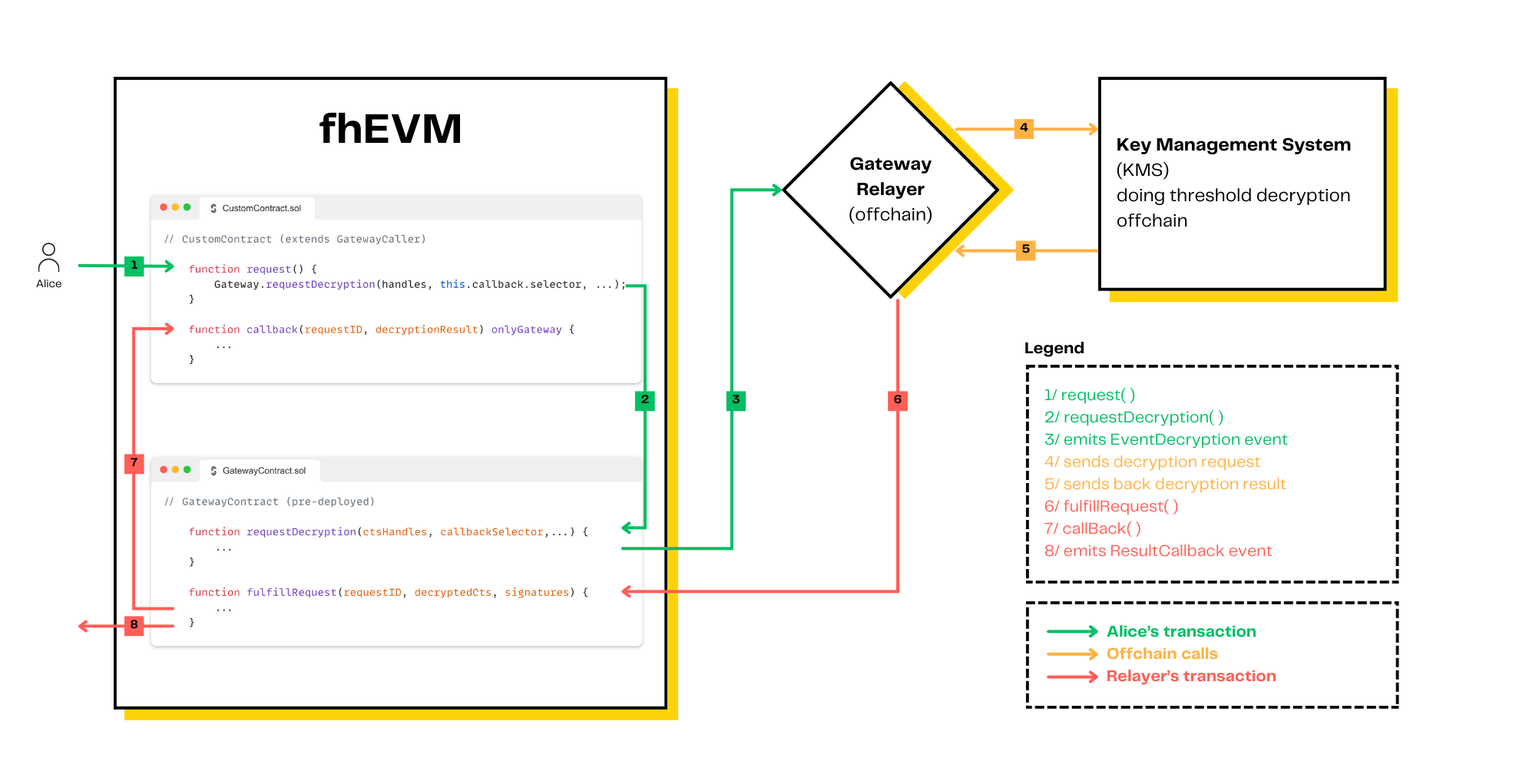

On fhevm blockchain - ZAMA team built, private key is owned by a Key Management Service (KMS). If the plaintext value is needed at some point, there are two ways to obtain it. Both methods are handled by a service called the Gateway. fhevm allow explicit decryption requests for any encrypted type. The values are decrypted with the network private key.

Kosmos Accounts give people access to Kosmos hosted services.

2) Kosmos Chat

Kosmos Chat is a group chat application. All of its components can be either self-hosted or connected to hosted services. No user data is ever locked into hosted silos.

Kredits are a system for tracking opensource project contributions, enabling and facilitating the fair and transparent use of project funds, as well as improving project management and governance. https://wiki.kosmos.org/Kredits

High-level overview

Similar projects/ideas

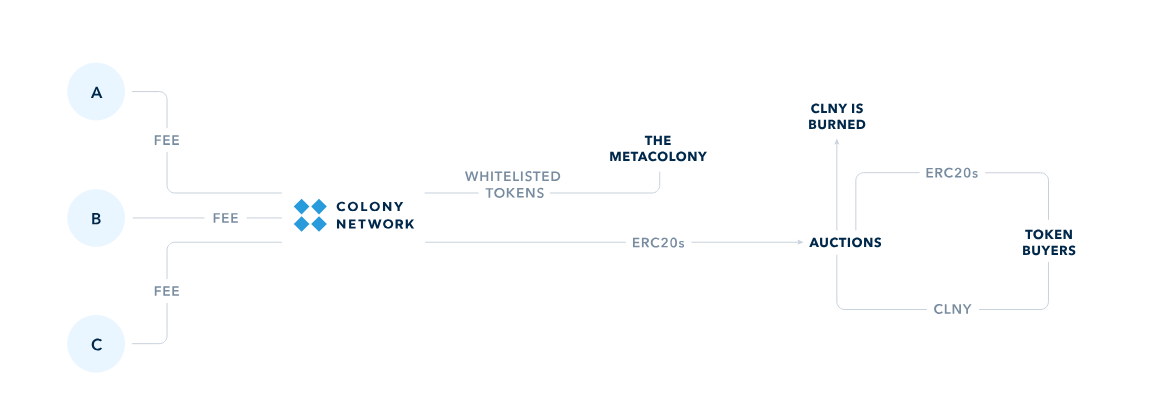

https://colony.io/ — Colony is a DAO which exists to make it easy for others to build DAOs. How Colony Makes Money

The Colony Network levies a small fee on Payments leaving a colony to an external address.

Fees paid in whitelisted tokens like USDC, USDT, WETH or xDAI go to the Metacolony to incentivise contributors.

Fees paid in other ERC20 tokens go to auctions where token buyers can purchase ERC20 tokens using CLNY, which is burned.

https://github.com/Commonfare-net/macao-social-wallet , https://freecoin.dyne.org/ — Freecoin is a set of tools to let people run reward schemes that are transparent and auditable to other organisations. It is made for participatory and democratic organisations who want to incentivise participation, unlike centralised banking databases.

https://www.gitcoin.co/ — Gitcoin Grants Program, we’ve distributed over $60M to early stage builders championing projects across DeFi, climate, open source and beyond.

https://shapeshift.com/ — ShapeShift champions the principles of permissionless access, trustless operations, privacy, and non-custodial asset management, providing users with a secure and autonomous digital currency management experience. ShapeShift supports 150+ different wallets including MetaMask, Ledger, xDeFi, WalletConnect, Coinbase, and Keplr.

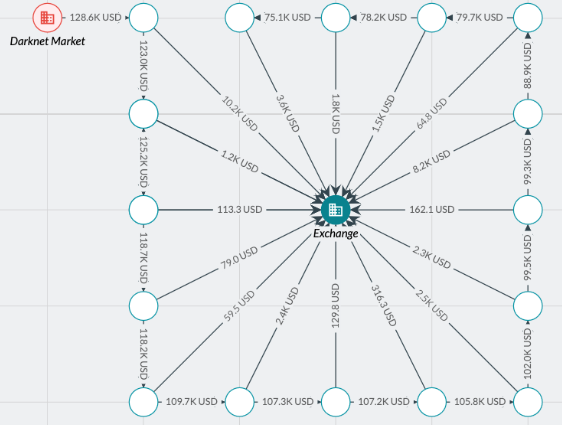

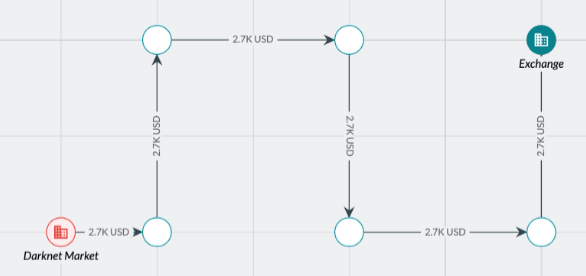

peeling chain 剥皮链 A peeling chain is a behavioral pattern where multiple repeated deposits are made at an exchange or service. A peeling chain pattern may suggest an attempt to stay below a certain KYC threshold to avoid detection. 剥皮链是指在交易所或服务平台上反复进行多次存款操作。剥皮链模式可能意味着试图保持在某个KYC阈值以下,以避免被检测到。

automated layering 自动分层 Automated layering, also called artificial hops, is a behavioral pattern that involves routing funds through multiple intermediate hops without any dilution of funds. An automated layering pattern may suggest an attempt to obfuscate the true source of funds by exploiting the fact that some screening programs will stop tracing at a certain number of hops. 自动分层,也称为人工跳跃,通过多次中间跳跃路由资金,而不稀释资金总额。自动分层模式可能表明企图利用某些筛查程序在一定跳跃次数后停止追踪的特点,来掩盖资金的真实来源。

mixer first funding 首次混币资助 Mixer first funding is a tactic used during high-profile exploits. Bad actors fund their attack addresses using a Mixer or Coin Swap Service to hide the original source of funds. While these services aren’t illegal in themselves, they allow users to obscure fund origins, which can facilitate illicit activities. This behaviour flags when addresses receive their first transaction from a mixer or low-KYC exchange.like Tornado Cash. 首次混币资助是在高调攻击事件中使用的策略。恶意行为者通过混币器或币交换服务为其攻击地址提供资金,以隐藏资金的原始来源。尽管这些服务本身不违法,但它们允许用户掩盖资金来源,可能助长非法活动。当地址接收到来自混币器或低KYC交易所的首次交易时,这种行为会被标记。例如,Tornado Cash。 在韩国,一起针对某知名区块链项目的攻击中,黑客利用混币器为攻击钱包地址提供初始资金。黑客通过混币服务掩盖了资金来源,然后对该区块链项目的智能合约漏洞进行了攻击,盗取了价值数千万美元的加密货币。

address poisoner 地址投毒者 Address Poisoner identifies addresses that conducted an address poisoning attack. Address poisoning, also known as address spoofing, is a scam where fraudsters create a fake wallet address resembling the user’s or one frequently used by them. Using this fake address, they send small amounts of cryptocurrency or NFTs to the user’s wallet, which ‘poisons’ the transaction history with deceitful transactions. They anticipate that the user, failing to notice the difference due to the address similarity, will unwittingly use the scam address for transactions - resulting in the loss of funds. 地址投毒者识别那些进行了地址投毒攻击的地址。地址投毒(也称地址欺骗)是一种骗局,骗子创建一个伪造的、与用户常用地址相似的钱包地址,并向用户的钱包发送少量加密货币或NFT,从而“污染”交易历史,使其充满欺骗性的交易记录。他们预期用户因地址相似而未能发现差异,从而在进行交易时不经意地使用了骗局地址,导致资金损失。 2022年底,美国一名诈骗者在某用户频繁使用的加密货币地址基础上,创建了一个仅在最后几位字符上不同的假冒地址。诈骗者利用这一相似地址,向受害者的钱包发送少量加密货币,希望受害者在未来的交易中误用该假冒地址,导致资金转入诈骗者控制的钱包。受害者没有仔细核对地址,误将价值数千美元的加密货币转入诈骗者的钱包。尽管事后发现了问题,但资金已无法追回。 1)诈骗者可以通过编写脚本,自动生成大量的地址,然后筛选出与目标地址相似的地址。由于每次生成的地址都是不同的,只要生成足够多的地址,总能找到一个与目标地址在某些位置上相似的地址。这个方法类似于“暴力破解”,需要大量的计算资源,但可以通过批量生成和筛选来实现。2)有些加密货币钱包允许用户使用一些工具(如Vanitygen)来生成“个性化”的地址,即地址的部分字符是可以指定的。这些工具允许用户设定地址的前缀或后缀,然后通过不断尝试生成满足条件的地址。例如,可以通过不断生成和筛选找到一个以特定字符或数字结尾的地址,从而与目标地址形成相似性。

exploiter 攻击者 Leverage this rule to mitigate interaction with addresses that have participated in a hack or exploit. 通过此规则,可以减少与曾参与黑客攻击或漏洞利用的地址之间的互动。

Ice phishing 冰钓式网络钓鱼 Ice phishing occurs when a user unknowingly allows a scammer to control their wallet. The scammer tricks the user into approving a transaction that looks safe, but in reality, the approval is granted to the scammer’s address hidden in transaction data. Once the approval is given, the attacker can take control over their digital assets. Leverage this rule to prevent interactions with addresses that have performed ice phishing attacks. 冰钓式网络钓鱼发生在用户在不知情的情况下允许诈骗者控制他们的钱包时。诈骗者诱骗用户批准一项看似安全的交易,但实际上,交易数据中隐藏的批准地址是诈骗者的。一旦批准,攻击者就可以控制用户的数字资产。通过此规则可以防止与执行冰钓式网络钓鱼攻击的地址进行交互。 2023年3月,英国某用户在一次空投活动中,批准了一项授权交易,实际上授权的是一个隐藏在交易数据中的恶意地址。该恶意地址由诈骗者控制,一旦获得授权,诈骗者迅速将用户的钱包中的代币转移至自己的钱包。受害者损失了价值超过50万美元的加密货币,而诈骗者利用多个分层账户迅速洗白这笔资金,避免了被追踪。

associated scammer address 关联诈骗者地址 Leverage this rule to mitigate interaction with addresses that have received funds from a known scammer. 通过此规则,可以减少与曾接收过已知诈骗者资金的地址之间的互动。

scammer deployed contract 诈骗者部署的合约 Leverage this rule to mitigate interaction with smart contracts deployed by known scammers. These contracts often promise high returns or false investments but are designed to siphon funds once the victim interacts with them. You can expand this section by discussing how smart contracts are audited (or not) and why code auditing practices could help detect scammer-deployed contracts early. 通过此规则,可以减少与已知诈骗者部署的智能合约之间的互动。这些合约通常承诺高回报或虚假投资,但其目的是在受害者与其互动后吸走资金。讨论如何审计智能合约(或不审计)以及为什么代码审计实践可以帮助及早发现诈骗者部署的合约来扩展此部分。

pig butchering 杀猪盘 Pig Butchering is a scam that utilizes deceptive communications to manipulate individuals into making fraudulent investments. This behavior identifies addresses that have received transactions suspected to be from Pig Butchering victims. This is accomplished by analyzing historical transactions made by victims of Pig Butchering. 杀猪盘是一种利用欺骗性沟通来操控个人进行虚假投资的骗局。该行为识别接收到疑似来自杀猪盘受害者交易的地址。这是通过分析杀猪盘受害者的历史交易实现的。 2023年7月,东南亚一个国际诈骗团伙通过社交平台接触受害者,利用情感交流和投资诱惑逐渐获取受害者的信任,随后引导受害者向所谓的“高收益投资项目”转账,实际上这些资金都进入了诈骗者控制的钱包。多个受害者损失金额高达数百万美元。受害者在察觉被骗后报案,但由于资金早已被分散转移至多个国家的加密货币账户,追查和追回难度极大。

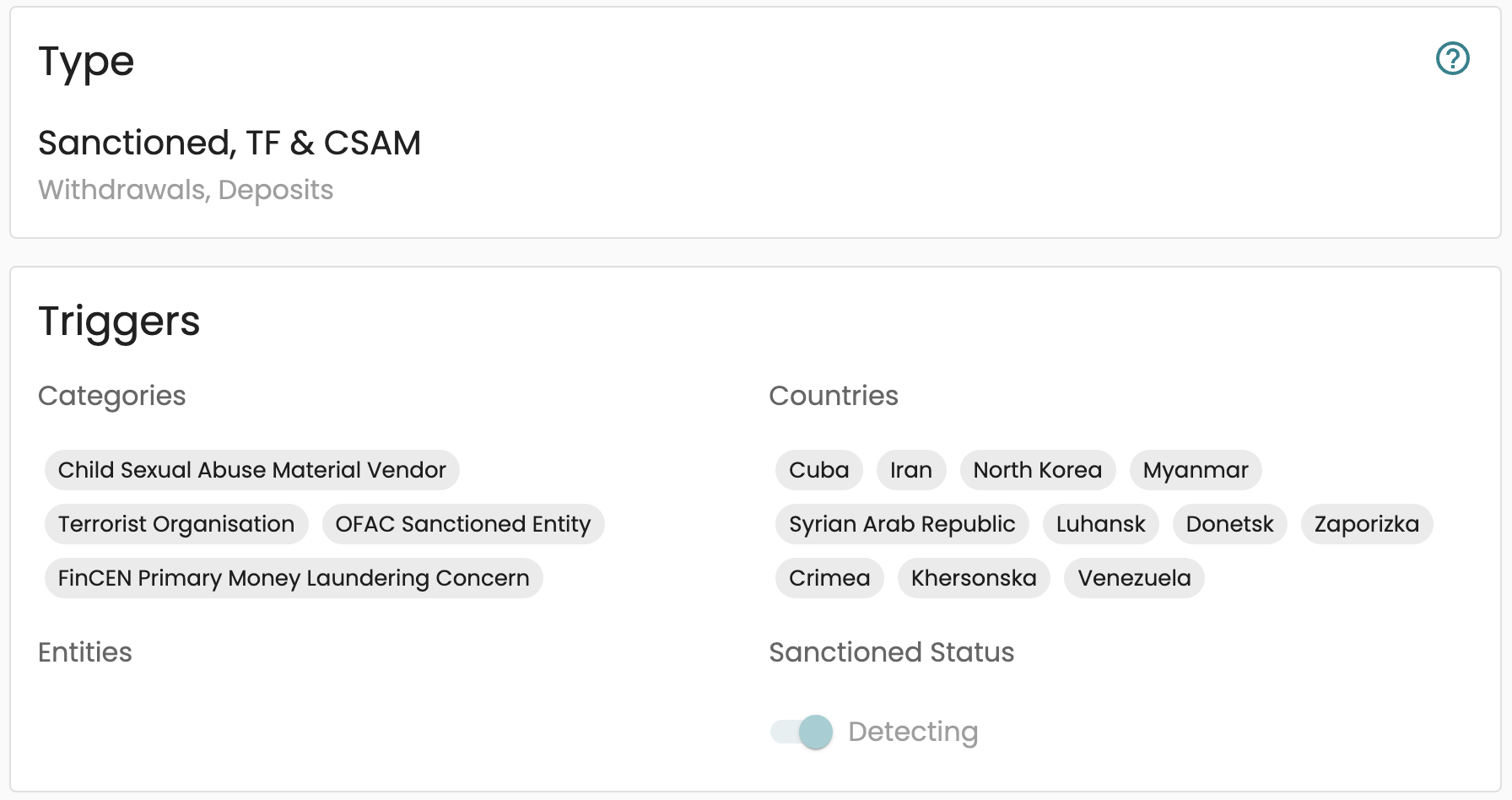

Exposure

Detect exposure to labeled entities using various risk triggers 意思是识别与某些特定类别的实体(如企业、个人或组织)之间的潜在风险关联。 系统通过多种风险触发器来检测用户或地址与这些标记的实体之间的交互情况。这些实体通常被标记为与特定的高风险活动相关:

1. Activist Fundraising (政治/社会运动筹款) 与政治或社会运动相关的筹款活动,可能涉及高风险或敏感的资金来源,存在被利用进行非法活动的风险。 Associated with political or social movement fundraising, potentially involving high-risk or sensitive fund sources, and could be used for illegal activities.

2. ATM (加密货币自动取款机) 加密货币ATM允许用户将加密货币兑换成现金或反向操作,因其匿名性和现金交易特性,可能被用于洗钱活动。 Cryptocurrency ATMs allow users to convert crypto into cash or vice versa. Due to their anonymity and cash-based transactions, they can be used for money laundering.

3. Authentication (身份认证服务) 涉及身份认证服务,可能存在身份欺诈和非法账户访问的风险。 Involves identity authentication services, which could carry risks related to identity fraud and unauthorized account access.

4. Bitcoin Faucet (比特币水龙头) 提供少量免费比特币的网站,可能被用于隐匿资金来源或洗钱。 Websites that distribute small amounts of free Bitcoin, potentially used to obscure the source of funds or launder money.

5. Bridge (跨链桥服务) 跨链桥服务用于在不同区块链之间转移资产,可能增加资金追踪的难度。 Cross-chain bridges allow asset transfers between different blockchains, which can complicate fund tracing.

6. Broker (经纪商/中介服务) 未经许可的金融中介服务,可能涉及非法金融活动或欺诈。 Unlicensed financial intermediaries, potentially involved in illegal financial operations or fraud.

7. Charity (慈善机构) 某些慈善机构可能被用于洗钱或掩盖非法资金流动。 Some charity organizations may be used for money laundering or concealing illegal fund flows.

8. Child Sexual Abuse Material Vendor (儿童性虐待材料供应商) 涉及儿童性虐待材料的交易,是严重的非法活动风险指示。 Involves the trade of child sexual abuse material (CSAM), a severe indicator of illegal activity.

9. Coin Swap Service (币种兑换服务) 币种兑换服务用于将一种加密货币兑换为另一种,可能被用于洗钱或隐藏资金来源。 Coin swap services exchange one cryptocurrency for another and may be used for money laundering or hiding the source of funds.

10. Credit Card Data Vendor (信用卡数据供应商) 非法出售信用卡数据的服务,常用于网络犯罪和欺诈。 Services that illegally sell credit card data, often used in cybercrime and fraud.

11. Criminal Organization (犯罪组织) 与已知犯罪组织相关的实体,这些组织涉及洗钱、勒索等非法活动。 Entities associated with known criminal organizations involved in activities such as money laundering, extortion, etc.

12. Dark Forum (暗网论坛) 暗网上的非法讨论平台,常用于信息交易和非法商品交易。 Illicit discussion platforms on the darknet, often used for information exchange and the trade of illegal goods.

13. Dark Market – Centralized (中心化暗网市场) 提供非法商品和服务的中心化暗网市场。 Centralized darknet markets offering illegal goods and services.

14. Dark Market – Decentralized (去中心化暗网市场) 去中心化的非法商品和服务交易市场,难以追踪和关闭。 Decentralized marketplaces for trading illegal goods and services, harder to trace and shut down.

15. Dark Service (暗网服务) 提供匿名代理、伪造文档等非法服务的平台。 Platforms providing illegal services such as anonymous proxy, forged documents, etc.

16. Dark Vendor Shop (暗网供应商店) 在暗网市场上设立的供应商店,提供非法商品或服务。 Vendor shops on darknet markets providing illegal goods or services.

17. Extortion (勒索) 通过威胁或强制手段获取资金,常见于勒索软件攻击中。 Obtaining funds through threats or coercion, commonly seen in ransomware attacks.

18. FinCEN Primary Money Laundering Concern (FinCEN主要洗钱关注对象) 被美国金融犯罪执法网络(FinCEN)认定为主要洗钱对象。 Entities identified by the U.S. FinCEN as primary money laundering concerns.

19. Gambling (赌博) 在线赌博服务,可能与资金洗白、欺诈有关。 Online gambling services, potentially associated with money laundering or fraud.

20. Known Criminal (已知犯罪分子) 已被确认与犯罪行为有关联的实体,涉及欺诈、盗窃等活动。 Entities known to be involved in criminal activities such as fraud, theft, etc.

21. Malware (恶意软件) 涉及恶意软件的交易,这些软件用于窃取资金或敏感信息。 Transactions involving malware used to steal funds or sensitive information.

22. Marijuana Vendor Shop (大麻销售店铺) 销售大麻的商店,在一些地区可能非法。 Shops selling marijuana, which may be illegal in certain jurisdictions.

23. Mixer (混币服务) 混币服务用于混淆加密货币的资金来源,常用于洗钱。 Mixing services used to obscure the source of cryptocurrency, often for money laundering.

What Kind of Service is CoinJoin? CoinJoin is a privacy-enhancing Bitcoin transaction which combines inputs from numerous users and returns multiple outputs of identical values. Unlike other mixing services, users maintain custody of their funds throughout this process. The uniformity of outputs is intended to obscure ownership of each UTXO and defeat the heuristic-based clustering algorithms used by law enforcement and blockchain investigators. For example, if four users input 2, 4, 6 and 8 BTC for a total of 20 BTC, the CoinJoin transaction would create 20 separate outputs each worth 1 BTC. The outputs would be apportioned to each user in the same amounts they originally contributed. Since every output has the same value, it should be impossible (in theory) to immediately discern which of the new bitcoin addresses are now controlled by each of the original four users.

24. OFAC Sanctioned Entity (OFAC制裁实体) 受到美国外国资产控制办公室(OFAC)制裁的实体。 Entities sanctioned by the U.S. Office of Foreign Assets Control (OFAC).

25. Phishing (网络钓鱼) 通过欺诈手段获取用户敏感信息(如私钥或登录凭证),常见于网络钓鱼攻击。 Fraudulently obtaining sensitive user information (e.g., private keys or login credentials), common in phishing attacks.

26. Ponzi Scheme (庞氏骗局) 一种非法的投资骗局,承诺高额回报,但实际上利用新投资者的资金支付旧投资者的收益。 An illegal investment scam promising high returns, but actually uses new investors’ funds to pay previous investors.

27. Privacy Wallet (隐私钱包) 注重隐私保护的钱包,可能被用于隐藏交易历史或资金流动。e.g., Wasabi Wallet。 Privacy-focused wallets designed to conceal transaction histories or fund flows. e.g., Wasabi Wallet.

28. Ransomware (勒索软件) 勒索软件攻击中使用的地址,受害者需支付赎金解锁被恶意加密的数据。 Addresses involved in ransomware attacks, where victims pay ransoms to unlock maliciously encrypted data.

29. Scam (诈骗) 涉及诈骗活动的实体或地址,这些地址可能用于网络钓鱼或其他形式的欺诈。 Entities or addresses involved in fraudulent activities, often used in phishing or other types of fraud.

30. Shielded (隐私交易) 通过隐私保护技术(如零知识证明)隐藏交易信息的工具。 Tools that use privacy-enhancing techniques (like zero-knowledge proofs) to hide transaction details.

31. Thief (盗窃) 涉及盗窃加密货币的地址,通常通过未经授权的访问或攻击行为。 Addresses involved in cryptocurrency theft, typically via unauthorized access or hacking.

32. Terrorist Organization (恐怖组织) 涉及恐怖组织的资金流动。 Transactions associated with terrorist organizations.

33. Human Trafficking (人口贩运) 与人口贩运相关的资金流动。 Transactions related to human trafficking activities.

34. Weapon Sales (武器销售) 非法武器销售相关的资金流动。 Transactions involving the illegal sale of weapons.

35. Drug Trafficking (毒品贩运) 与非法毒品交易相关的资金流动。 Transactions related to the illegal drug trade.

36. Sanctioned Countries (受制裁国家) 与受国际制裁国家的交易,可能违反国际法。 Transactions with entities from sanctioned countries, potentially violating international law.

37. Shell Companies (空壳公司) 被用于洗钱或隐藏非法资金来源的空壳公司。 Shell companies used for money laundering or hiding illegal fund sources.

38. High-Risk Jurisdictions (高风险司法管辖区) 与高腐败或监管薄弱的国家或地区的交易,可能增加洗钱风险。 Transactions with countries or regions known for weak regulations or high corruption, increasing money laundering risks.

39. Fraudulent ICO (欺诈性ICO) 假冒的初始代币发行,承诺高额回报但无实际项目支持。 Fake Initial Coin Offerings (ICOs) that promise high returns but have no real project backing.

40. Illegal Content (非法内容) 传播或交易非法内容(如盗版、暴力、仇恨言论),这些行为通常违反法律。 The distribution or trade of illegal content (e.g., pirated material, violence, hate speech), which typically violates the law.

41. Illicit Marketplace (非法市场) 从事非法商品或服务交易的市场,这些市场往往涉及洗钱、毒品或武器交易。 Marketplaces that deal in illegal goods or services, often involving money laundering, drug trade, or weapons transactions.

42. Money Mule (资金骡子) 通过第三方账户转移非法资金的活动,这些账户通常不知情或自愿参与。 Involves the transfer of illicit funds through third-party accounts, where the account holders may be unaware or willingly participate.

43. Ponzi-like Scheme (类庞氏骗局) 与庞氏骗局类似的投资骗局,承诺高额回报但实际上以新的投资者资金支付旧投资者的收益。 A fraudulent investment operation similar to a Ponzi scheme, promising high returns while using new investors’ money to pay earlier investors.

44. Privacy Coin (隐私币) 设计用于隐藏交易细节的加密货币,虽然保护用户隐私,但也可能被用于非法活动。 Cryptocurrencies designed to conceal transaction details, while enhancing user privacy, may also be used for illicit activities.

45. Ransomware Payment (勒索软件支付) 向勒索软件攻击者支付赎金的交易,用以解锁被恶意加密的数据。 Transactions made to ransomware attackers to unlock maliciously encrypted data.

46. Sanctioned Individual (受制裁个人) 与受国际或政府制裁的个人进行交易,可能违反制裁法律。 Transactions with individuals under international or government sanctions, potentially violating sanction laws.

47. Suspicious Transaction (可疑交易) 异常或可疑的交易行为,可能与洗钱、欺诈或其他非法活动相关。 Transactions that appear abnormal or suspicious, potentially linked to money laundering, fraud, or other illicit activities.

48. Terrorist Financing (恐怖主义融资) 为恐怖组织提供资金的行为,通常通过加密货币隐秘进行。 The act of providing financial support to terrorist organizations, often facilitated covertly through cryptocurrency.

49. Unlicensed Money Service Business (无牌照货币服务业务) 未经许可的货币兑换或转账服务,可能涉及洗钱或非法金融活动。 Unlicensed currency exchange or transfer services, potentially involved in money laundering or illegal financial activities.

50. Whale Transaction (巨鲸交易) 涉及大量加密货币交易,可能引起市场波动或被用于非法资金转移。 Transactions involving large amounts of cryptocurrency, potentially affecting market stability or used for illicit fund transfers.

51. Front-Running (抢跑交易) 涉及利用未公开的市场信息,在合法交易被确认之前抢先执行交易,导致市场操纵或不公平的交易环境。 Front-running involves using non-public market information to execute trades before legitimate trades are confirmed, leading to market manipulation or unfair practices.

52. Pump-and-Dump (拉高出货) 一种市场操纵手段,操纵者人为抬高加密货币的价格,吸引散户投资者购买,随后抛售手中的大量持仓。 A form of market manipulation where perpetrators artificially inflate the price of a cryptocurrency to attract retail investors, then sell off their large holdings.

53. Wash Trading (刷单交易) 交易者通过自己在不同账户间反复买卖相同资产,制造虚假交易量,操纵市场价格。 Traders repeatedly buy and sell the same asset between their own accounts, creating fake trading volume to manipulate market prices.

54. Regulatory Arbitrage (监管套利) 利用不同司法管辖区的监管差异,通过选择监管较宽松的地区进行交易,规避合规要求。 Taking advantage of regulatory differences across jurisdictions by trading in regions with looser regulations to avoid compliance requirements.

=============== the risks below are not in the list of Elliptic and TRMLAB =============== ================= 以下风险没有包含在 Elliptic and TRMLAB 的范围内 =================

55. Fake News Manipulation (假新闻操纵) 散布虚假消息,影响市场情绪和资产价格,从中获利或导致市场动荡。 Spreading false information to manipulate market sentiment and asset prices, either for profit or to destabilize the market.

56. Tax Evasion (逃税) 使用加密资产来隐瞒收入,逃避税收,特别是在多个国家拥有资产的情况下。 Using cryptocurrencies to hide income and evade taxes, especially when assets are held across multiple countries.

57. Insider Trading (内幕交易) 未公开的内部信息被用于个人利益相关的交易,可能违反证券法。 Using non-public insider information for personal gain in trading, potentially violating securities laws.

58. Peer-to-Peer (P2P) Market Risks (点对点市场风险) 在P2P交易市场上,用户可以绕过银行或正规金融机构进行交易,增加欺诈或非法交易的风险。 On peer-to-peer markets, users can bypass banks or formal financial institutions, increasing the risk of fraud or illicit transactions.

59. Layer 2 Protocol Risks (Layer 2协议风险) 涉及Layer 2扩展方案的风险,这些方案用于提高区块链交易的可扩展性,但可能缺乏充分的安全性或合规措施。 Risks related to Layer 2 scaling solutions, which aim to improve blockchain transaction scalability but may lack robust security or compliance measures.

60. Flash Loan Exploits (闪电贷攻击) 使用无抵押的闪电贷款,在单个交易中操纵市场或智能合约,进行非法获利。 Using uncollateralized flash loans to manipulate the market or smart contracts within a single transaction for illicit profit.

61. Smart Contract Exploits (智能合约漏洞利用) 利用智能合约中的漏洞或缺陷,执行未授权的资金转移或操纵合约行为。 Exploiting vulnerabilities or flaws in smart contracts to carry out unauthorized fund transfers or manipulate contract behavior.

62. NFT Fraud (NFT欺诈) 与非同质化代币(NFT)相关的欺诈行为,包括伪造稀有资产、洗钱或欺骗性交易。 Fraud involving Non-Fungible Tokens (NFTs), including forgery of rare assets, money laundering, or deceptive transactions.

63. Liquidity Pool Exploitation (流动性池利用) 通过操纵流动性池的算法或规则非法获利,导致投资者或交易者损失。 Illegally profiting by manipulating the algorithms or rules governing liquidity pools, causing losses to investors or traders.

64. DeFi Protocol Risks (去中心化金融协议风险) 去中心化金融(DeFi)平台的风险,包括智能合约漏洞、治理攻击、流动性枯竭等。 Risks associated with decentralized finance (DeFi) platforms, including smart contract vulnerabilities, governance attacks, and liquidity exhaustion.

65. Unregulated Stablecoins (无监管稳定币) 某些稳定币未受监管,可能在破产、赎回失败或资产透明性不足的情况下带来系统性风险。 Some stablecoins are unregulated, potentially posing systemic risks in the event of insolvency, redemption failures, or lack of transparency.

What Kind of Information Can be Traced?

The twin goals of cryptocurrency forensics and asset tracing — identify the perpetrator, and find their funds — are pursued through several areas of analysis and fact-finding:

Attribution Data: Blockchain intelligence tools collect and analyze ownership attribution information for thousands of entities, which can be used to de-anonymize blockchain addresses for identification of criminals and investigative subjects. These systems rarely provide personally identifying information (PII) for individual owners of specific cryptocurrency assets, but may identify known associations with criminal groups or fraud schemes, as well as transactions with other relevant entities, such as exchanges and fiat off-ramps where criminal proceeds are converted to cash.

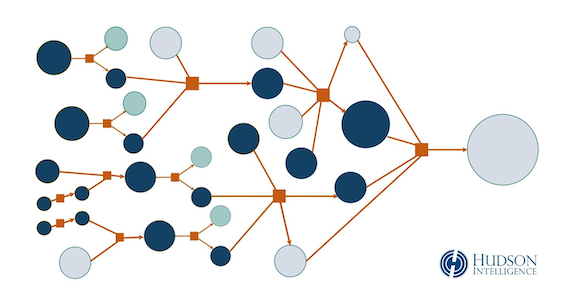

Transaction Mapping: Transactional data is converted into visual maps and flowcharts, showing interactions by the subject with known exchanges and other entities, tracing financial transfers to their ultimate endpoints. Visual mapping makes it much easier to recognize patterns, such as layering and peel chains, commonly used for money laundering. Expert investigators use powerful tools that automate mapping and evidence collection. This approach is more efficient and more effective than blockchain search engines or open-source explorers that require manual review of ledger entries.

Cluster Analysis: A cluster is a group of cryptocurrency addresses that are controlled by the same person or entity. Expanding the focus of an investigation from one address to a larger cluster can dramatically increase the amount of available evidence for de-anonymization and asset tracing. Cluster analysis can also be used to determine if any linked addresses have a substantial current value or UTXO.

Subpoena Targets: Commercial cryptocurrency exchanges, decentralized finance (DeFi) firms, and virtual asset service providers that comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations typically require verification of customer identity for new accounts. This makes them a highly valuable resource for de-anonymizing subjects who have used their services to buy, trade, hold, or cash-out cryptocurrency. Personally identifying information for registered owners of addresses and wallets – as well as their banking details – may be obtainable through civil subpoenas or criminal warrants.

Current/Historical Value: Cryptocurrency addresses with significant value are critical indicators for financial recovery. They may be appropriate targets for seizure warrants by criminal prosecutors, or garnishment during civil judgment enforcement.

Total Transactions: Volume of cryptocurrency transactions can signify the potential size of a fraud scheme and number of victims. Complaints to law enforcement typically receive more attention when a crime syndicate has harmed numerous people. Larger schemes may also be appropriate for class action suits in civil court.

Risk Profiling: Automated risk-scoring is conducted through advanced algorithms that trace activity of target address(es) and identify associations with known entities such as exchanges, mixers, peer-to-peer exchanges, sanctioned parties, ransomware rings, and darknet markets.

IP Address: Privacy-piercing metadata is collected through blockchain surveillance systems, which run networks of nodes that “listen” and “sniff” for Internet Protocol (IP) addresses associated with certain transactions. IP addresses, when available, may provide information regarding the geographical location of the subject at the time of the transaction.

How to create a Finance business Risk Rule?

Combination of the risk rules as a business rules as below:

Rules as best example (Elliptic)

Category

Description

Example

Activist Fundraising

Entities that have (a) either been convicted of a crime directly related to extremist activity or (b) have been identified and verified to have incited prejudice, violence and/or serious crimes. Elliptic maintains a rigorous and objective internal process when determining whether an entity should be ascribed to this label, based on the above conditions.

Pankkake (Anonymous Far Right Donor)

ATM

An automated teller machine at which cryptoassets can be sold and purchased for fiat currency; similar to a traditional bank-operated ATM.

ATM brands include SatoshiPoint, Lamassu, GenesisCoin

Authentication

A service that allows users to prove their unique identity without having to enter in their login credentials when accessing a particular website, thus increasing security.

Civic

Bitcoin Faucet

A type of website that at one time gave away Bitcoin for free. Now these websites usually reward users in the form of Bitcoin for completing tasks such as captchas.

Moonbit

Blockchain

Addresses linked to the operation of the blockchain.

TON Foundation

Bridge

A contract or service used to transfer assets from one blockchain to another.

Ren

Broker

An entity involved in the buying and selling of cryptoassets on behalf of clients. Unlike an exchange, a broker does not have an order book.

Cumberland Mining

Charity

A non-profit or charitable organisation that accepts Bitcoin donations.

US Luge Foundation

Child Sexual Abuse Material Vendor

A vendor offering Child Sexual Abuse imagery for cryptoasset payment.

Coin Swap Service

A crypto-to-crypto conversion service with fixed exchange rates that does often not require a user to login or any KYC.

ChangeNOW

Credit Card Data Vendor

An online carding shop, providing illicit credentials and other illicit personal financial information.

JokerStash.store

Criminal Organisation

A group of multiple individuals involved in organised crime.

The Shadow Brokers

Crypto-Exchange

An exchange where customers can only trade cryptoassets in exchange for other cryptoassets.

Poloniex

Dark Forum

A TOR-only accessible online discussion forum

DNM Avengers

Dark Market - Centralised

A TOR-only accessible marketplace selling illegal goods and services with a centralised infrastructure. The marketplace has its own wallet infrastructure and holds users keys on it. Individuals making and receiving purchases interact with the marketplace, rather than with the seller or buyer directly.

Dream Market

Dark Market - Decentralised

A TOR-only accessible marketplace selling illegal goods and services with a decentralised infrastructure. The marketplace does not have its own wallet infrastructure. Individuals making and receiving purchases interact directly with the seller or buyer.

Wall Street Market

Dark Service

An illicit service, including hacking, wallet, and web hosting services.

PinPays

Dark Vendor Shop

A TOR-only accessible individual vendor shop on a dark marketplace that sells illegal goods and services.

Euroarms

Data

A vendor that provides data for the end user, such as details regarding the bitcoin address owner, such as username and email address.

BitcoinWhosWho

De-Fi

A decentralised financial platform, usually run through a smart contract.

MakerDAO

Decentralised Exchange

A decentralised service that provides crypto-to-crypto exchange services, such as Bitcoin to Ethereum.

Uniswap

Entertainment

A vendor that provides streaming, TV, films, and other entertainment services.

Escrow

A vendor that provides escrow services for a transaction between two parties.

Safe Lock

Exchange

A centralised service that provides fiat-to-crypto exchange services, such as USD to bitcoin. The exchange may also provide crypto-to-crypto exchanges services, such as Bitcoin to Ethereum.

Coinbase

Extortion

The use of force or threats to obtain funds from an individual or multiple individuals.

Ashley Madison Extortion

Financial Services

A financial services organisation providing financial services, such as loans, bonds, and derivatives products.

Bitbond

FinCEN Primary Money Laundering Concern

FinCEN uses this designation when it has identified a financial institution, jurisdiction, or type of account as being of significant risk for money laundering or the financing of terrorism.

Bitzlato - FINCEN Section 9714 - January 18 2023

Forum

An online discussion forum.

Reddit

Gambling

Gambling services.

BetChain

Hardware Wallet

A physical hardware wallet to store cryptoassets; located often on a separate external hard drive with the purpose of providing additional wallet security.

Bitcoin Paper Wallet

High Transaction Fee

A transaction involving a higher than average transaction fee to miners, suggesting possible loss or criminal activity.

A group investment provider, such as a cryptoasset venture operator or multi-level marketing scheme.

Coinsilium

Known Criminal

A Known Criminal is a known individual involved in illicit activity. A Known Criminal is often linked to a Criminal Organisation.

Ross Ulbricht and Carl Mark Force

Law Enforcement

A known law enforcement entity.

FBI

Layer 2

A blockchain scaling solution built on a “Layer 1” blockchain, typically enabling faster transactions with lower fees, while retaining the security of the Layer 1 protocol.

Lightning Network

Malware

Software that is intended to damage or disable computers and computer systems.

Trickbot

Marijuana Vendor Shop

A marijuana dispensary, registered in a regulated jurisdiction.

Speedweed

Merchant

Online licit merchants or vendors.

Mypayingcryptoads

Microtransactions Service

Website promoting microtransactions, for example freelance work, web plugins generating cryptoassets.

coinworker

Mine

Newly minted cryptoassets which are created as part of the mining/validating process.

The bitcoin which is paid to miners as the block reward and transaction fees

Miner

A service that mines and generates new cryptoassets.

BTC.TOP

Misc Service

A miscellaneous uncategorized service, vendor, or organisation.

Coinfirm

Mixer

A service that allows for cryptoassets mixing or tumbling in order to anonymise funds. Used for both privacy purposes and also for laundering funds.

Chip Mixer

News

An online news publishing service.

ProPublica

NFT Marketplace

A marketplace enabling creators to sell NFTs to its users.

OpenSea

OFAC Sanctioned Entity

An entity sanctioned by the Office of Foreign Assets Control (OFAC) of the US Department of the Treasury.

Garantex Europe OU - OFAC SDN - 5 Apr 2022

Outsourcing Provider

A website promoting freelance opportunities.

coinworker

Payment Services Provider

A service offering the ability to accept online payments through a variety of payment methods, including cryptoassets.

BitPay

Peer to Peer Exchange

A platform on which individual buyers and sellers can exchange cryptocurrency for other payment types with one another.

Phishing

A form of fraud in which a message sender attempts to trick the recipient into divulging important personal information like a password or bank account number, transferring money or installing malicious software. Usually, the sender pretends to be a representative of a legitimate organisation.

A form of fraud in which belief in the success of a nonexistent enterprise is fostered by the payment of quick returns to the first investors from money invested by later investors.

Jetcoin

Privacy Wallet

A crypto wallet that offers features helping users to avoid de-anonymization on the blockchain. This could be by allowing them to participate in coinjoin transactions, or by providing a built-in mixer service, among others.

Wasabi wallet

Ransomware

A type of malicious software from cryptovirology that threatens to publish the victim’s data or perpetually block access to it unless a ransom is paid.

WannaCry 2.0

Reported Loss

Purported loss of cryptoasset often due to destruction or a fork. Unlike a theft, the funds associated with a loss are no longer accessible, as a loss often involves the destruction of private keys.

October 2011 Mt. Gox Loss

Research Chemicals

Bulk chemical retailers for laboratory use only. However, in practice, research chemicals are often used to produce illicit drugs.

Buckled.eu

Scam

Any other type of fraudulent scheme.

Prodeum

Shielded

A shielded address uses cryptographic techniques to obscure on-chain information such as addresses and amounts

Software Development

A software development organisation.

GIMP

Software Wallet

An intangible software wallet to store cryptoassets, located on an online platform, individual’s computer, or external hard drive.

MyBitcoin

Terrorist Organisation

An organisation involved in terrorism or related activity.

ISIS

Thief

Recipient of stolen funds.

Stolen CoinSecure Funds

Token

Tokens are a representation of a particular asset or utility, that resides on top of another blockchain, such as Ethereum. Tokens can represent a range of fungible assets, such as property, to assets that are intangible, like Cryptokitties, and cryptoassets, like EOS.

EOS

Token Sale

A Crowdsale, pre-sale, or otherwise sale associated with the launch of a Token or other cryptoasset.

Atlant Token Crowdsale

Trading Platform

An exchange software and services provider. This entity does not operate exchanges but provides the software to operate them.

Alphapoint

User

A forum or social media user.

Niktitan132

Unknown

An “unknown” entity or category means the address is not labeled in the Elliptic system. This means we do not recognize the address as being controlled by any specific entity.

Validator

A Validator for a Ledger-based currency.

Venture Capital

A venture capital organisation working with startups, early-stage, and emerging companies that have been deemed to have high growth potential.

Alter VC

VPN Vendor

A vendor that provides Virtual Private Networks (VPN) services.

These are client-submitted incidents involving fraudulent activity, such as the use of fraudulent credit card data. It is placed within the Thief category but the identity of the actor is unknown eg. Fraud Incident - 1171161288

Thief

Blacklisted Address

A token issuer has blacklisted these addresses. Elliptic does not have any information regarding why the address is blacklisted. Contact the issuer for more details, eg. USDT Blacklisted Address - 57492936